Property Newsletter | January 2023

Buyer's market in 2023

as house price inflation likely to be below inflation

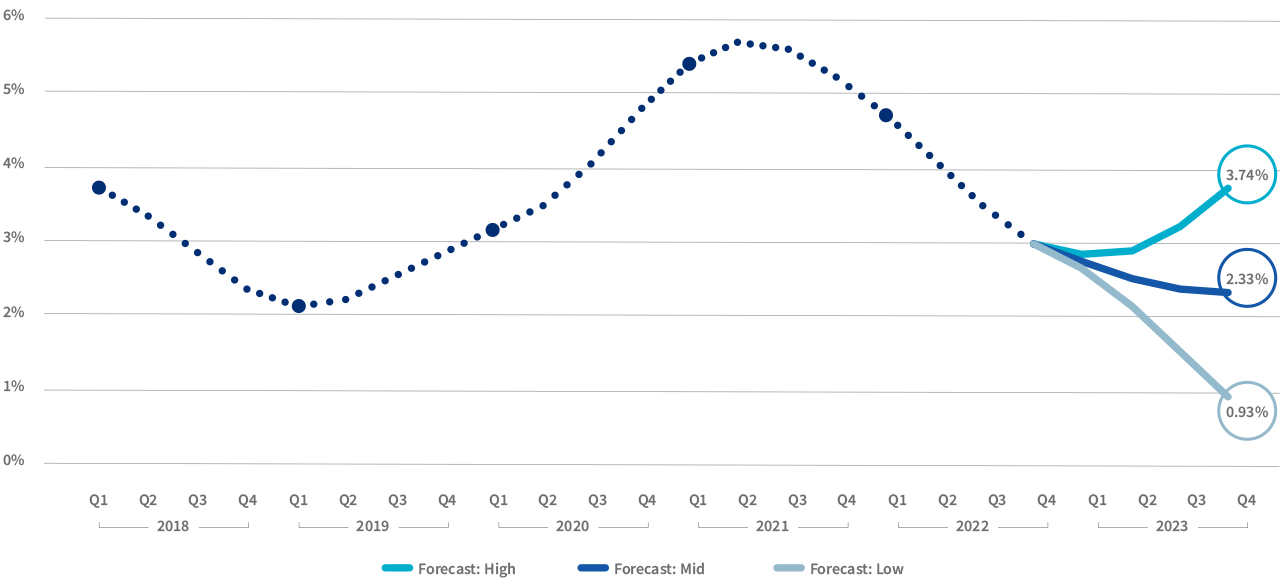

Lightstone’s scenarios put HPI from 0.9% to 3.7%

House price inflation (HPI) in South Africa’s residential property market in 2023 will be shaped by local and global challenges – but mostly will feel the pain of the country’s stagnating economy and grow less than inflation.

Paul-Roux De Kock, Chief Analytics Officer at Lightstone, provider of comprehensive data, analytics and systems on property, automotive and business assets, said Lightstone’s three scenarios suggested HPI in SA would likely come in between 0.9% (low) to 2.3% (mid) or 3.7% (high).

With no end in sight for SA’s electricity woes and increasing water outages, the South African Reserve Bank (SARB) recently increased interest rates by 25 basis points and adjusted its GDP growth forecast to just 0.3% for 2023, down from its previous estimate in November of 0.6%. The bank expects growth for 2022 to come in at 2.5%.

The Consumer Price Index (CPI) and core inflation have significantly diverged over the past 18 months, with CPI ending 2022 at 7.2% and core inflation – which excludes the impact of the volatile fuel price driven by Russia’s war with Ukraine – ending at 4.9%. “We have used the more predictable core inflation rate in our forecasts”, said De Kock.

National house price inflation

Mid HPI scenario – 2.3%

With the base line GDP growth expectation of 0.3%, Lightstone expects the SARB will take a moderate approach to interest rate hikes with interest rates rising slowly by a total of 100 basis points for the year. “We expect core inflation to drop to 4% in such a scenario, and HPI is forecasted to continue the slow decline we’ve seen for more than a year and end 2023 at 2.3%”, he said.

High HPI scenario – 3.7%

Under a scenario where the economy sufficiently recovers to support GDP growth of 1.1%, Lightstone expects core inflation to climb to 5.5% with interest rates increasing by 200 basis points. “Under such a scenario we forecast HPI to bounce back in the second quarter and end 2023 at 3.7% with strong upward momentum going into 2024.”

Low HPI scenario – 0.9%

If the economy stagnates at 0% GDP growth and core inflation drops to 3%, De Kock said SA might experience an accelerated decline in HPI, ending the year at 0.9% with a negative trajectory for 2024. Under such a scenario the SARB might stop the upward interest rate cycle sooner (only increasing it by 50 basis points for the year) offering some consolation to homeowners with outstanding debt.

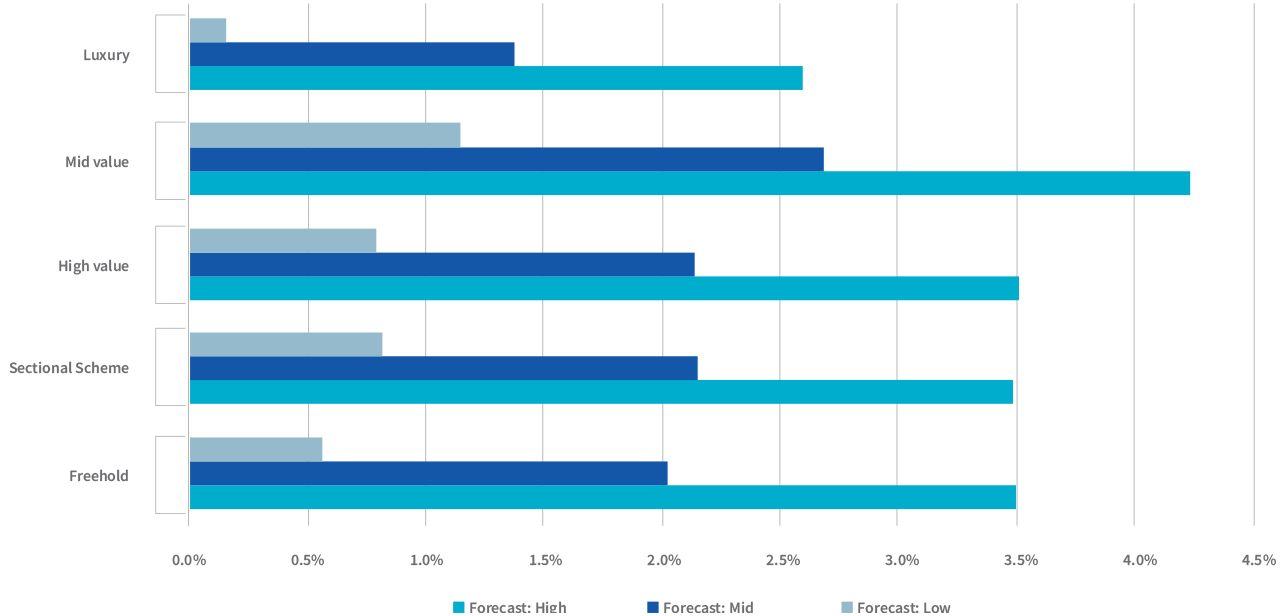

Mid value market segment to weather economic storms best

The mid value market segment should be more resilient than other segments, in all these scenarios, as it will gain from the more active informal economy as well as activity from buyers out of the higher value segments wanting to downscale.

We expect HPI in this market segment to only drop to 1.2% in our low HPI scenario and it has the potential to reach 4.2% HPI in our high HPI scenario.

Segment forecast – 2023 Q4

Higher value outstanding mortgages in sections of the Luxury market segment have seen this segment more negatively affected by the upward interest rate cycle and Lightstone expects this to continue under the Mid and Low HPI scenarios.

“In our High HPI scenario we expect HPI in this market to start recovering sooner than the lower value market segments, but coming off a low base we see limited upside potential in 2023”, said De Kock.

During the course of 2022 the Freehold and Sectional Scheme HPI have converged around the national average. De Kock said Lightstone expected this trend to continue with Sectional Schemes being slightly more resilient in the Low and Mid HPI scenarios.

Modelling inputs up to December 2023

.png)

.png)

.png)

.png)