Auto Insights Newsletter | April 2024

Is the entry segment really growing?

Segment share of Passenger market constant but choice down and price up over last 10 years

It’s the first time vehicle buyers in South Africa have less brand and vehicle type choice than 10 years ago – and they are paying more for their Entry segment vehicle. And, while the Entry segment has maintained its share of the Passenger market over the last 10 years, it has not shown the kind of growth it perhaps should have.

Although some brands have made significant strides with respect to their ranking within the segment, it would seem they have been taking up the slack left by the withdrawal of others, rather than adding sales to the segment.

In addition, the Weighted Average Price (WAP) of an Entry segment vehicle has grown faster than the market average – between 2014 and 2018 the WAP of an Entry vehicle was around 45% of the WAP for the market, whereas between 2019 and 2023, this is now closer to 50% – another indication that the cheapest vehicles on the market might not be the primary focus of the South African consumer.

What’s changed?

The Entry segment’s ranking within the Passenger market segment and the composition of the segment itself have changed.

Over the past decade, this segment has been dominated by the likes of the Volkswagen Polo Vivo, Toyota Etios, Hyundai Grand i10, Kia Picanto and Renault Kwid.

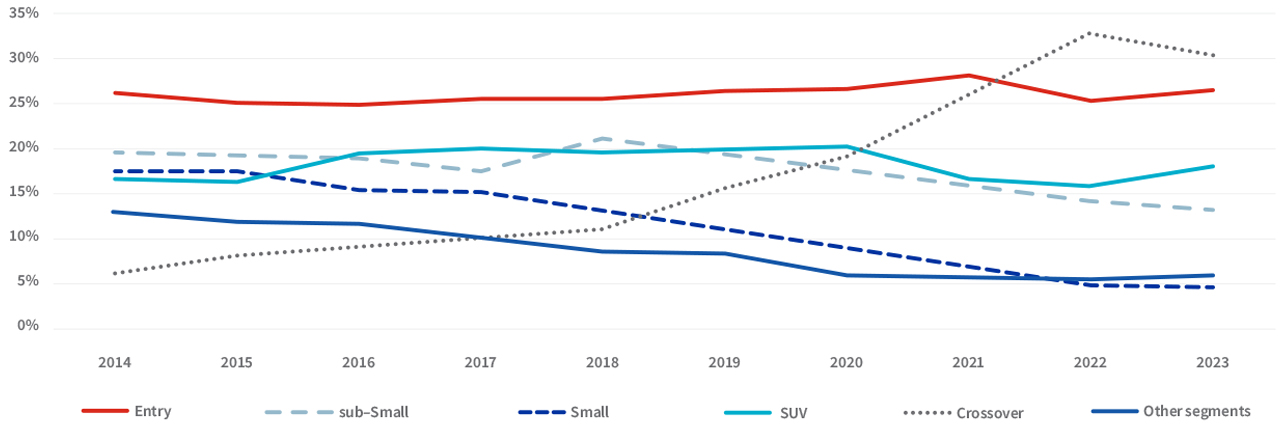

In 2014, (see graph below) the Entry segment was the biggest selling segment in the Passenger market, with 26% market share, followed by the sub-Small and Small segments, with 20% and 18% share respectively. The Entry segment held this position until 2022 when it was usurped by the fast-growing Crossover segment, which had only reached the second spot in 2021.

Passenger segment share: 2014 – 2023

The Entry segment’s share of market has remained reasonably constant over the past 10 years: it was 26% of the Passenger market in 2014 and ended 2023 with a 27% share. The lowest it fell to was 25% in 2016, and the highest it reached was 28% in 2021, the year when South Africa began its recovery from Covid.

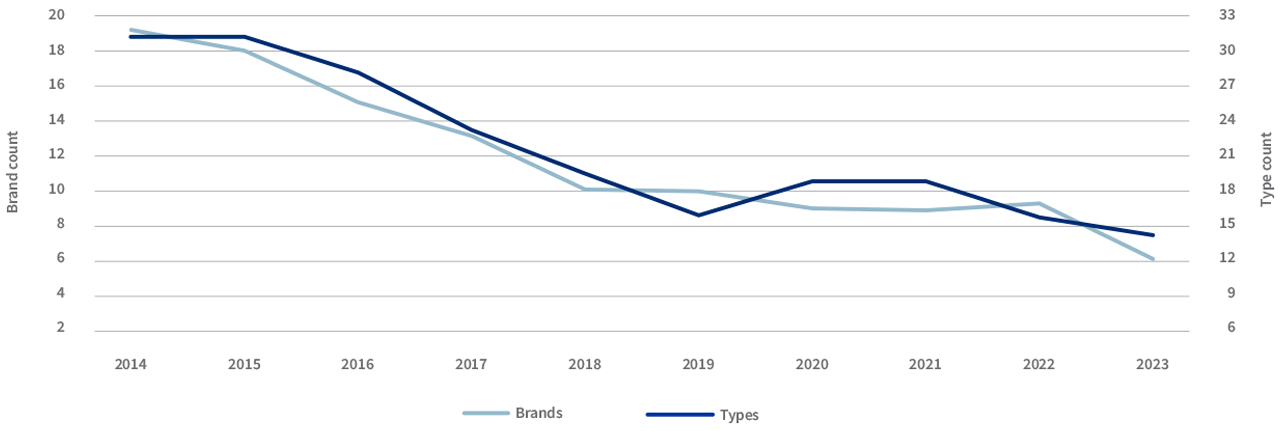

But while the Entry level has maintained a consistent share of the Passenger market, the number of competitors within the segment has fallen.

In 2014 there were 19 different brands selling 31 separate vehicle types in this segment. Chevrolet, Ford, Hyundai, Renault, Toyota and Volkswagen all reported more than 5 000 units sold over the year. By 2019 there were 10 makes and 16 types in the segment, and those that fell away included Chery, Chevrolet, Citroen, FAW, Fiat, GWM, Mitsubishi, Proton and Tata.

Entry segment vehicle mix: 2014 – 2023

By 2023 a further four brands had dropped out of the segment (Datsun, Ford, Honda and Peugeot), leaving just six remaining, providing 14 vehicle types. This means the Entry segment brand pool has contracted by 68% over the last 10 years, and the number of vehicle types has shrunk by 55%.

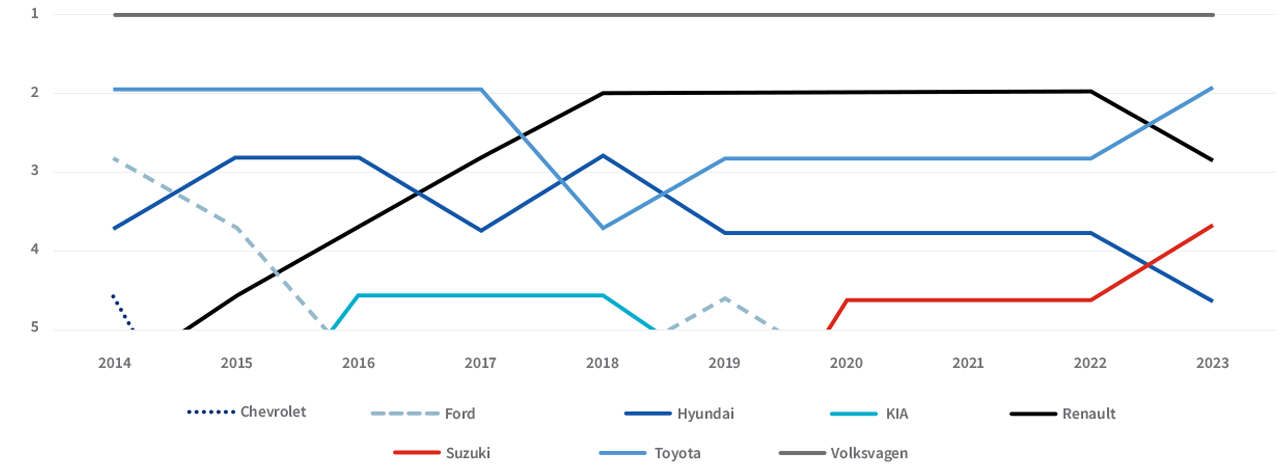

Volkswagen has kept its spot at the top of the brand standings in the Entry segment over the last 10 years, with Toyota and Renault spending five years each in second place (Toyota held that position in 2023). The annual Top 5 over the decade has also included Suzuki, Hyundai, Kia, Chevrolet and Ford (the latter two obviously no longer in the current mix).

Entry segment brand position: 2014 – 2023

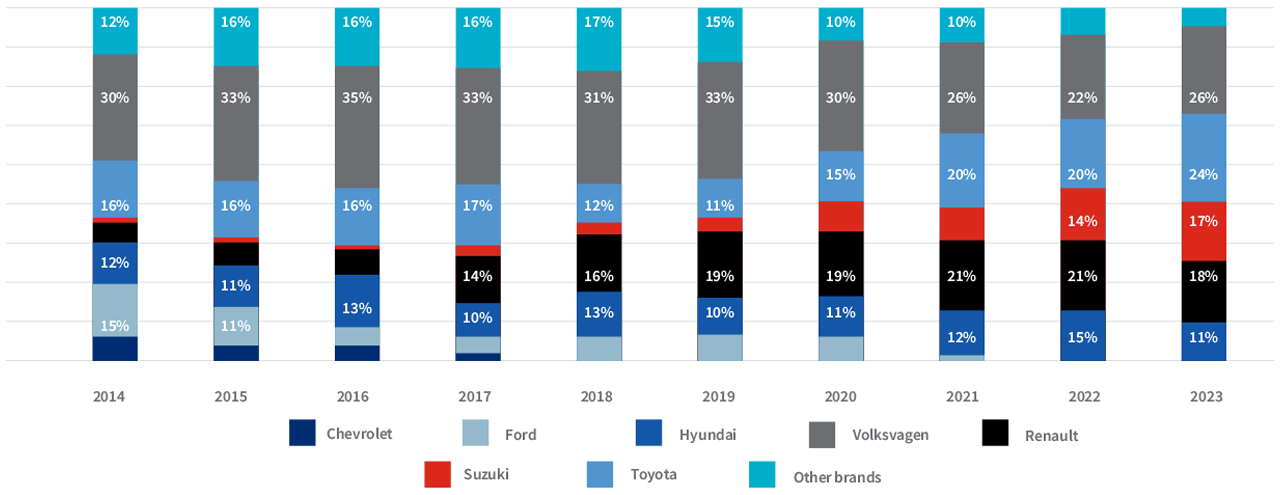

Volkswagen’s segment share in 2014 was 30% and has varied between 22% (2022) and 35% (2016) with 2023 coming in at 26%. After recording a 16% segment share in 2014, Toyota has fluctuated between a low of 11% (2019) and a high of 24% (2023).

Suzuki and Renault have been the big growth stories in the segment, with the latter having a 6% segment share in 2014 and growing this to 18% in 2023 (marginally down on the 21% they recorded in 2021 and 2022). Suzuki’s growth in segment share has been even more dramatic, climbing from 1% in 2014 to 17% in 2023.

Entry segment brand share: 2014 – 2023

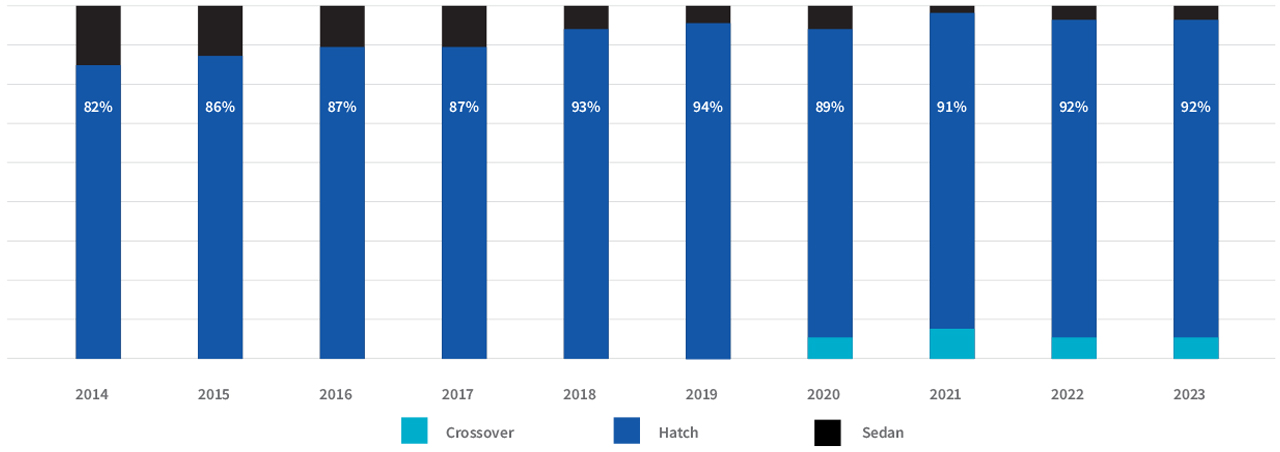

Hatchback bodyshape as popular as ever

The 3-door and 5-door hatchback have been a staple of the Entry segment, and have continued to consolidate their position over the last 10 years. In 2014 the hatch had an 82% share of sales in the Entry segment, with the balance being sedans. In 2023 this share grew to 92%, while the sedan share shrunk to 3%, and the nascent entry-level Crossover shape enjoyed a 5% share.

Entry segment bodyshape share: 2014 – 2023

Weighted Average Price balloons over 10 years

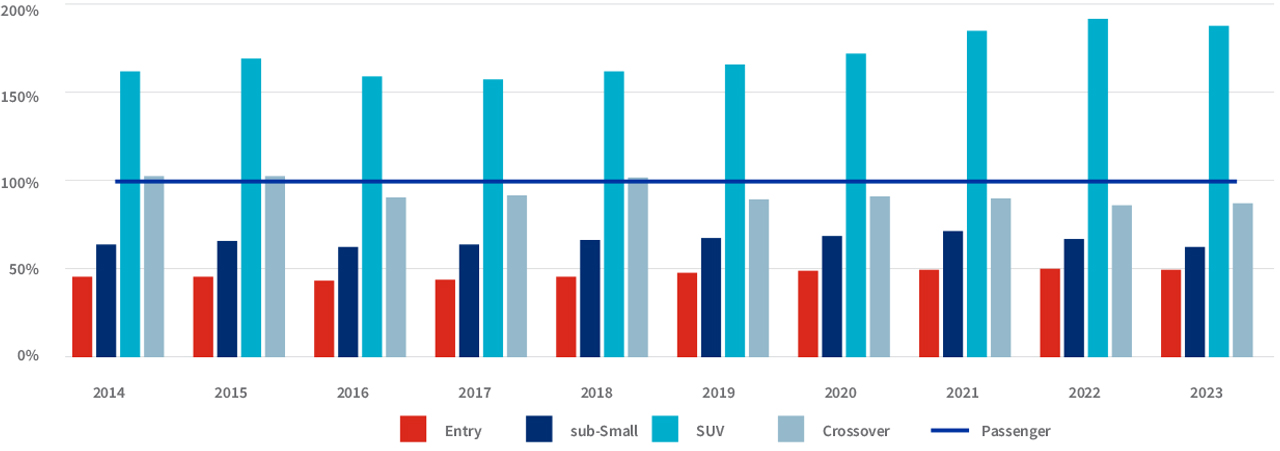

The WAP of an Entry segment vehicle in 2023 was 72% higher than in 2014, compared to a 57% increase for a new vehicle in the Passenger market. Both the Crossover and sub-Small segments saw lower WAP increases over the 10 years than the market as a whole, at 33% and 53% respectively, while the MPV segment also beat out the Entry segment with its WAP increasing by 59%.

Selected segments WAP ratio to Passenger WAP: 2014 – 2023

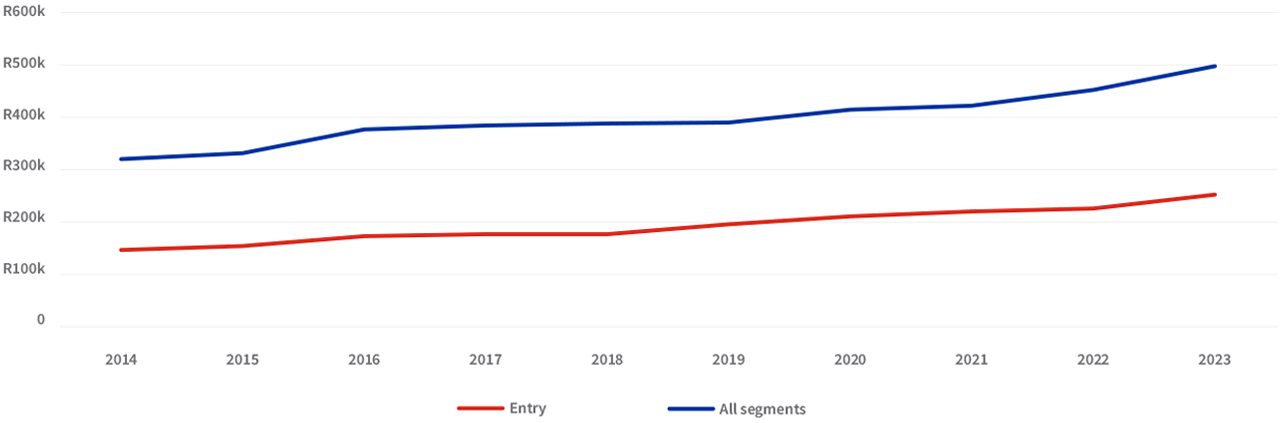

Entry segment Weighted Average Price: 2014 – 2023

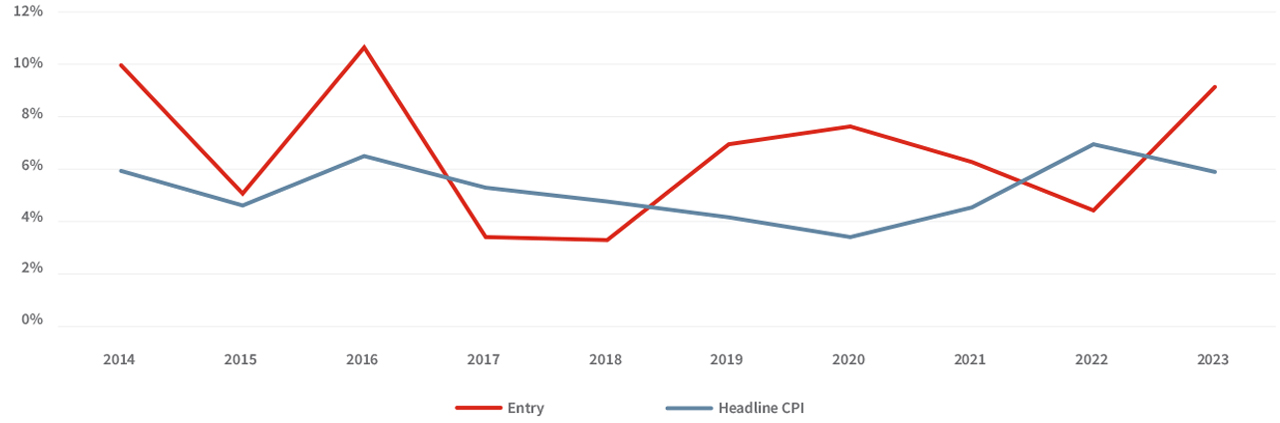

When comparing the change in WAP for the Entry segment to the change in Headline Consumer Inflation as released by StatsSA, it is interesting to note that in seven of the last 10 years, growth in Entry segment WAP has exceed that of CPI.

Entry segment WAP increase vs Headline CPI: 2014 – 2023

.png)

.png)

.png)

.png)